Thesis Weekly_Week 23: SpaceX Opened at $2.1 Trillion. Chips Lost $1.3 Trillion. Adobe Tripled Its AI Revenue.

The market is not leaving technology.

If you haven’t explored our previous research, you may revisit some of our earlier due diligence reports and thematic notes below. Each piece reflects the same thesis-driven framework we apply across every investment case.

1. Market Lens

📊 Market Lens | Weekly Snapshot Week Ending: June 12, 2026

S&P 500:7,431.46(WoW +0.6%)

VIX:17.68(-3.83 pts)

10Y Treasury:4.485%(-5.1 bps)

WTI:$84.88(WoW -6.3%)

Brent:$87.33(WoW -3.4%)

Gold:$4,238.80(WoW -2.9%)

DXY:99.75(WoW -0.3%)

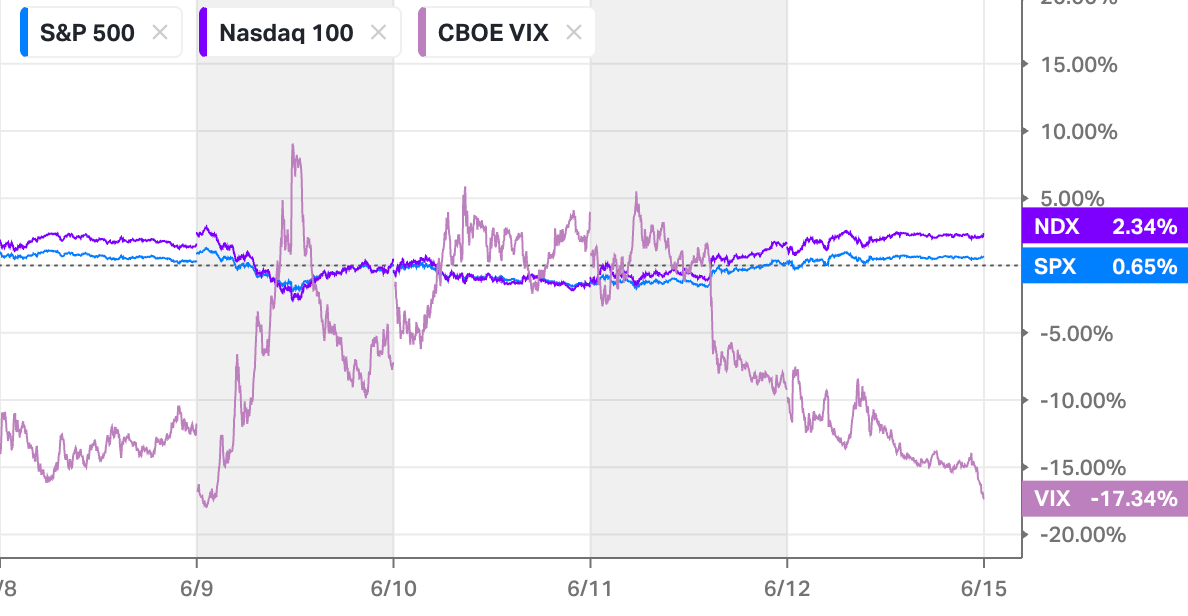

The S&P 500 ended the week up 0.6%. VIX fell from 21.51 to 17.68. Oil dropped 6.3%. By every surface measure, the week resolved cleanly after last week’s chip-driven dislocation. Look at the inputs that produced that resolution and the picture is considerably more complicated.

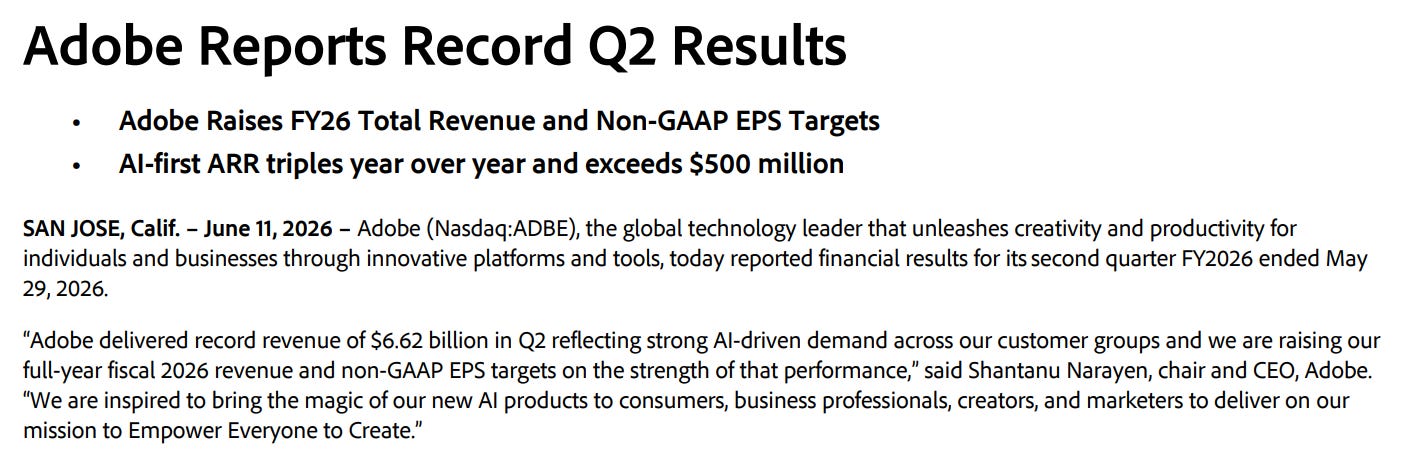

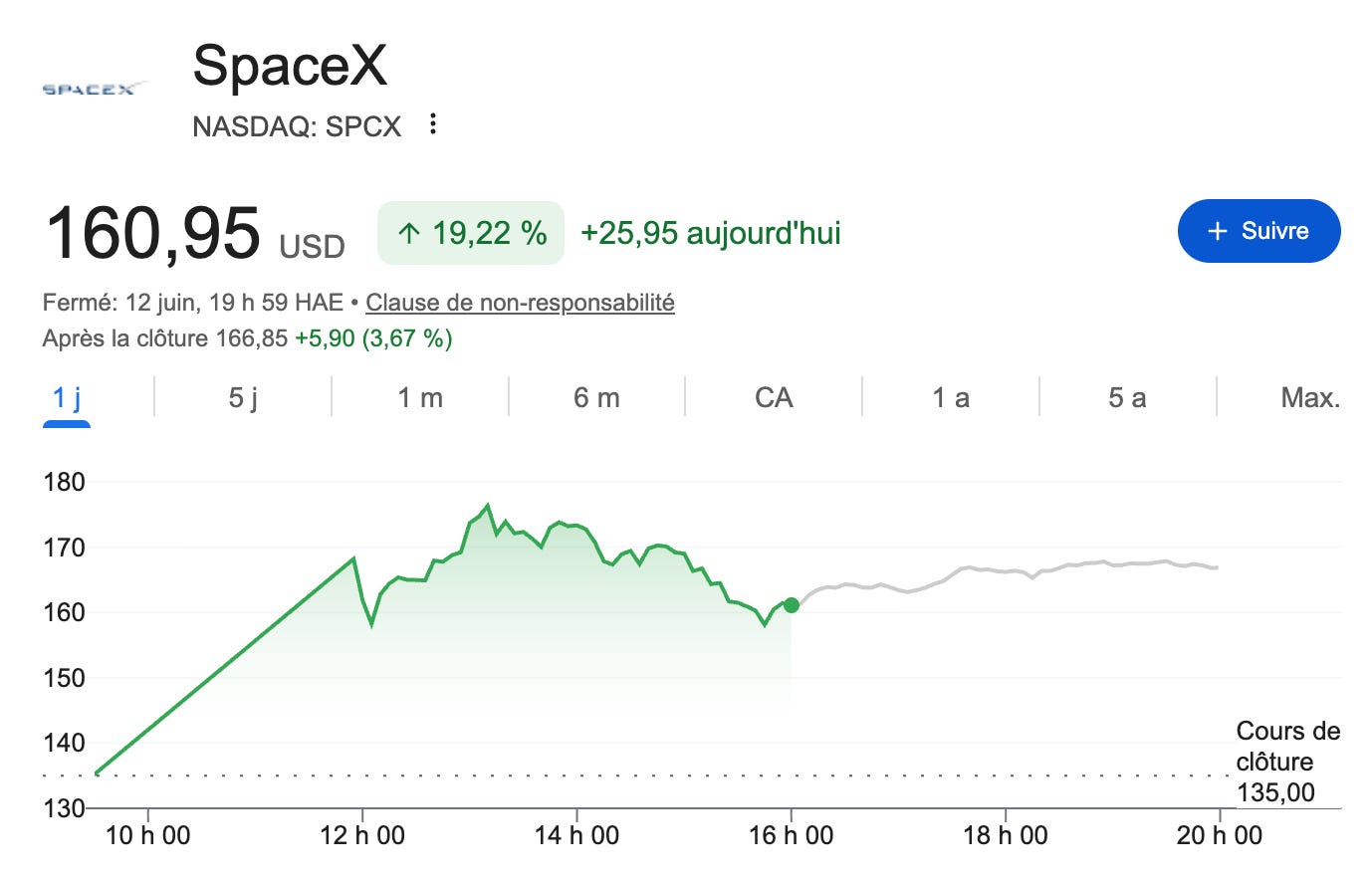

The week’s most consequential event arrived on Thursday June 11 in a compressed window of several hours. The White House announced it was formally canceling planned strikes on Iranian oil infrastructure and confirmed that a sovereign framework agreement with Tehran, covering a ceasefire framework and the reopening of the Strait of Hormuz, had received approval from Iran’s highest leadership level. The agreement is in final signing stages. Within the same afternoon, SpaceX priced its IPO at $135 per share, raising $75 billion and implying a valuation of $1.75 trillion. Adobe reported Q2 results of $6.62 billion in revenue, a record, with AI-first ARR tripling year-over-year and crossing $500 million. WTI immediately dropped 2.6% on the Iran news. The S&P 500 surged 1.8% on the day. The Nasdaq jumped 2.5%. Three separate market-moving events landed simultaneously, and the net effect was the largest single-day rally in nearly two months.

But the underlying macro data released earlier in the week told a different story. May CPI, published Wednesday, came in at 4.2% year-over-year, the highest print since 2023 and materially above April’s 3.8%. Core CPI rose to 2.9%. The inflation that has been described as transitory, energy-driven, and war-related for three months is now running at the highest annual rate of this entire cycle. On the same day, the 10-year Treasury yield was, in the words of CNBC, “steady even after data showing highest inflation since 2023.” That steadiness is the tell. A bond market that does not sell off on a 4.2% CPI print is a bond market that is already pricing in a resolution to the energy shock, not dismissing the inflation. The bond market saw Thursday’s Iran deal coming before it was announced.

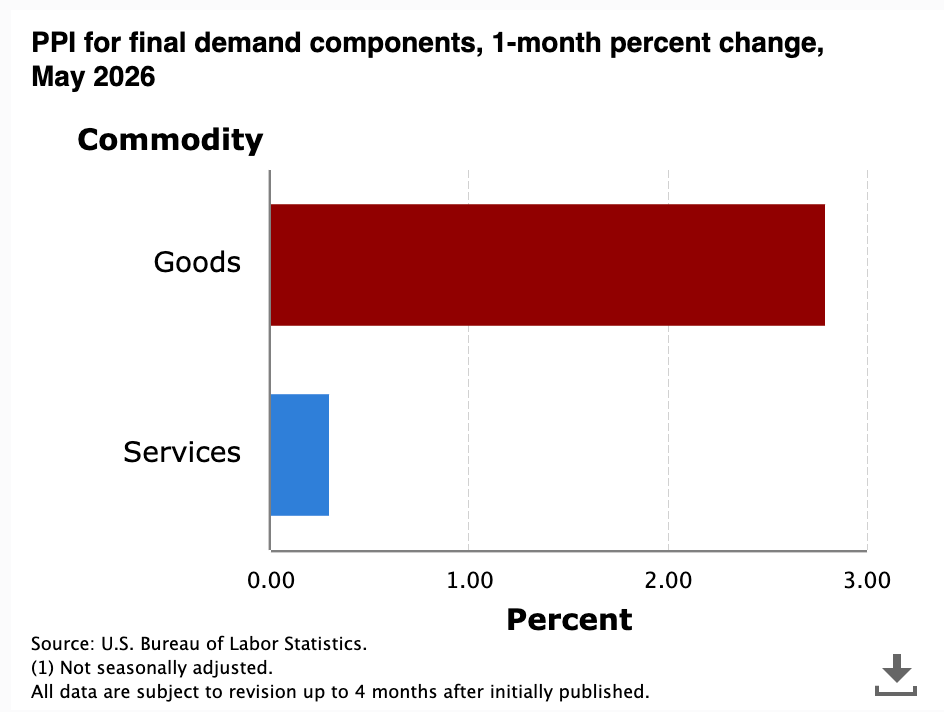

PPI released the following day confirmed what the supply chain has been building toward for months. May PPI rose 6.5% year-over-year, the largest increase since November 2022, with core PPI reaching 5.1%. These numbers represent the wholesale cost of production before retail inflation. They are a leading indicator. The pipeline from PPI to CPI runs with a three to six month lag. If PPI is at 6.5% and CPI is at 4.2%, the direction of travel for consumer prices is not ambiguous. It is upward, unless something disrupts the supply chain that is driving it. The Iran deal is that disruption. Goldman Sachs, reading the same data, pushed its first expected Fed rate cut to June 2027 and warned that a hike before year-end carries a higher probability than the market currently prices. Kevin Warsh delivers his inaugural address as Federal Reserve Chairman on Monday morning. The market will be listening for every word.

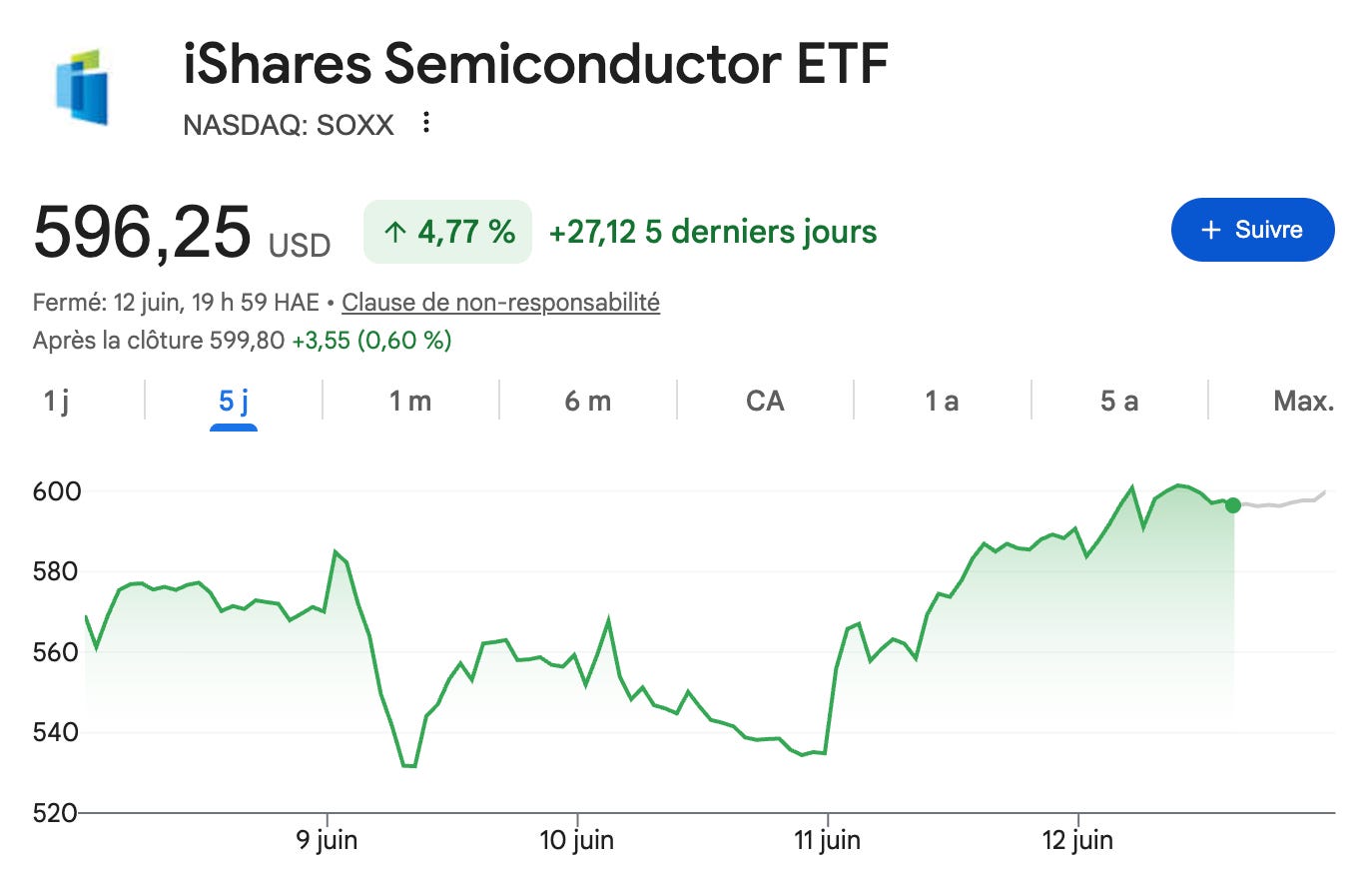

The chip sector spent the week absorbing the aftershock of Broadcom’s earnings. When Broadcom capped its full-year AI semiconductor revenue guidance at $56 billion, a figure far below the $100 billion the most aggressive sell-side models had been running, the repricing was immediate and brutal. AMD, Intel, and their peers shed a combined $1.3 trillion in market capitalization over the week. The divergence within technology became sharper. CoreWeave, confirmed this week as a new member of the Nasdaq 100, gained 5% while the chip index fell. The capital rotation is precise: money is leaving businesses that pitch AI story while moving toward businesses that have signed contracts for AI compute delivery. The market is applying an increasingly granular filter to what counts as AI exposure.

Adobe reported Q2 FY2026 results on Thursday evening that contained two separate narratives in a single press release. The operational story was unambiguous: record revenue of $6.62 billion, up 11% year-over-year, AI-first ARR tripling to above $500 million, non-GAAP EPS of $5.96 growing 18%, and a full-year guidance raise. The AI monetization that the thesis required is manifesting in contracted ARR, not pipeline. The corporate governance story was more complicated: CFO Dan Durn announced his departure effective June 15, four days after the earnings release, with no advance notice to investors. Adobe enters the second half of its fiscal year without a permanent CEO, Narayen having announced his intention to step down once a successor is named in March, and now without a permanent CFO. The stock fell 5.5% in after-hours trading. The business is performing. The institution around it is in an unusual state of transition that the market is discounting in the multiple.

SpaceX opened for trading on Friday June 12 and its market capitalization immediately crossed $2.1 trillion, surpassing the combined valuations of ExxonMobil, Bank of America, and Coca-Cola. The company carries a first-quarter net loss of $4.28 billion and allocates approximately $2.5 billion per quarter to AI infrastructure spending. The valuation arithmetic requires either a fundamental belief that Starlink’s global satellite broadband business will generate revenue at a scale that has never existed in the telecommunications industry, or a belief that the SpaceX brand, the xAI integration, and the Musk factor together justify a premium that financial modeling alone cannot produce. The IPO’s 30% retail allocation, unprecedented at this scale, suggests the company’s bankers understood that the latter is doing significant work in this equation.

This Week’s Signal: CPI hit 4.2%. Oil fell 6%. The market rallied. The Iran deal is doing more for inflation than the Federal Reserve has been able to do in six months of holding rates. Kevin Warsh speaks Monday.

Module 2: Portfolio Desk

This Week’s Focus

Two deliberate actions this week moved in opposite directions on purpose. AMD was partially trimmed after appreciating approximately 300% from its initial entry, returning the position to its original sizing of ~1% and recovering the capital that price drift had added without a corresponding thesis upgrade. That capital was partially redeployed into MSFT, which was added to 3.5%, reflecting continued conviction in the enterprise AI monetization layer as the chip sector’s Broadcom-driven selloff draws a sharper line between infrastructure storytelling and contracted revenue. Adobe delivered record Q2 results with AI-first ARR tripling to above $500 million, then announced its CFO’s surprise departure four days later. The business is compounding. The governance situation is not.

Defensive Anchors

V, TMUS, WM, ROL, LIN, COST | Hold No material developments across the defensive tier. The Iran peace deal framework, if signed, is the most direct macro catalyst for V through cross-border volume normalization and for COST through supply chain cost reduction. ROL’s non-discretionary demand thesis was reinforced by the CPI 4.2% print: in a sustained high-inflation environment, the services that cannot be deferred are precisely the ones that compound. All six positions hold against stated theses with monitoring variables unchanged.

Core Compounders

Berkshire Hathaway (BRK.B) | Hold | ~6.5% The $10 billion Alphabet private placement disclosed last week and the Iran deal progress this week represent two separate signals pointing toward the same conclusion: the macro environment that has justified holding $397 billion in cash is beginning to shift. Energy-driven inflation may have peaked. If Hormuz reopens, the Fed’s primary justification for maintaining restrictive policy weakens. Berkshire’s deployment timing becomes a live analytical question rather than a theoretical one. Monitoring variable: any additional capital deployment announcement in the weeks following the Iran deal signing.

AutoZone (AZO) | Hold | ~4.5% No material developments. CPI at 4.2% and a 7%+ auto loan rate are structural tailwinds for the aftermarket parts thesis: new vehicle ownership remains prohibitively expensive for the median American household, extending the fleet age that drives AZO’s commercial segment. Monitoring variable: Q4 FY2026 results expected late June.

Kinsale Capital (KNSL) | Hold | ~5.0% No material developments. Thesis intact. Monitoring variable: Q2 combined ratio.

Copart (CPRT) | Hold | ~3.0% | Under Review No new earnings this week. Q4 FY2026 results are the final data point before a formal position decision. The May Q3 beat on pricing confirmed the moat is intact. Volume recovery is the remaining open variable. Monitoring variable: Q4 total loss frequency and unit volume.

Blue Chip

Microsoft (MSFT) | Action: Add | Allocation: ~3.5% | Category: Blue Chip