If you haven’t explored our previous research, you may revisit some of our earlier due diligence reports and thematic notes below. Each piece reflects the same thesis-driven framework we apply across every investment case.

For a closer look at how these principles translate into real positions, explore the 👉 Sample Portfolio — a demonstration of thesis-driven allocation and disciplined compounding.

Artificial intelligence has triggered a recurring question in capital markets and enterprise strategy:

if large language models can generate code, summarize documents, automate workflows, and interpret data, does that make traditional Software-as-a-Service platforms obsolete?

The narrative is seductive. If AI can build applications dynamically, why maintain subscription-based software layers? If natural language becomes the interface to everything, does structured enterprise software still matter?

The short answer is no. AI does not replace SaaS in a structural sense. It changes the interface layer, compresses certain forms of labor, and redistributes value within the software stack. But the economic foundations of SaaS, particularly in enterprise environments, remain intact.

The more interesting question is not whether AI replaces SaaS, but how AI redefines where value accrues within SaaS ecosystems.

1. What SaaS Actually Is

To understand whether AI replaces SaaS, one must first define SaaS accurately.

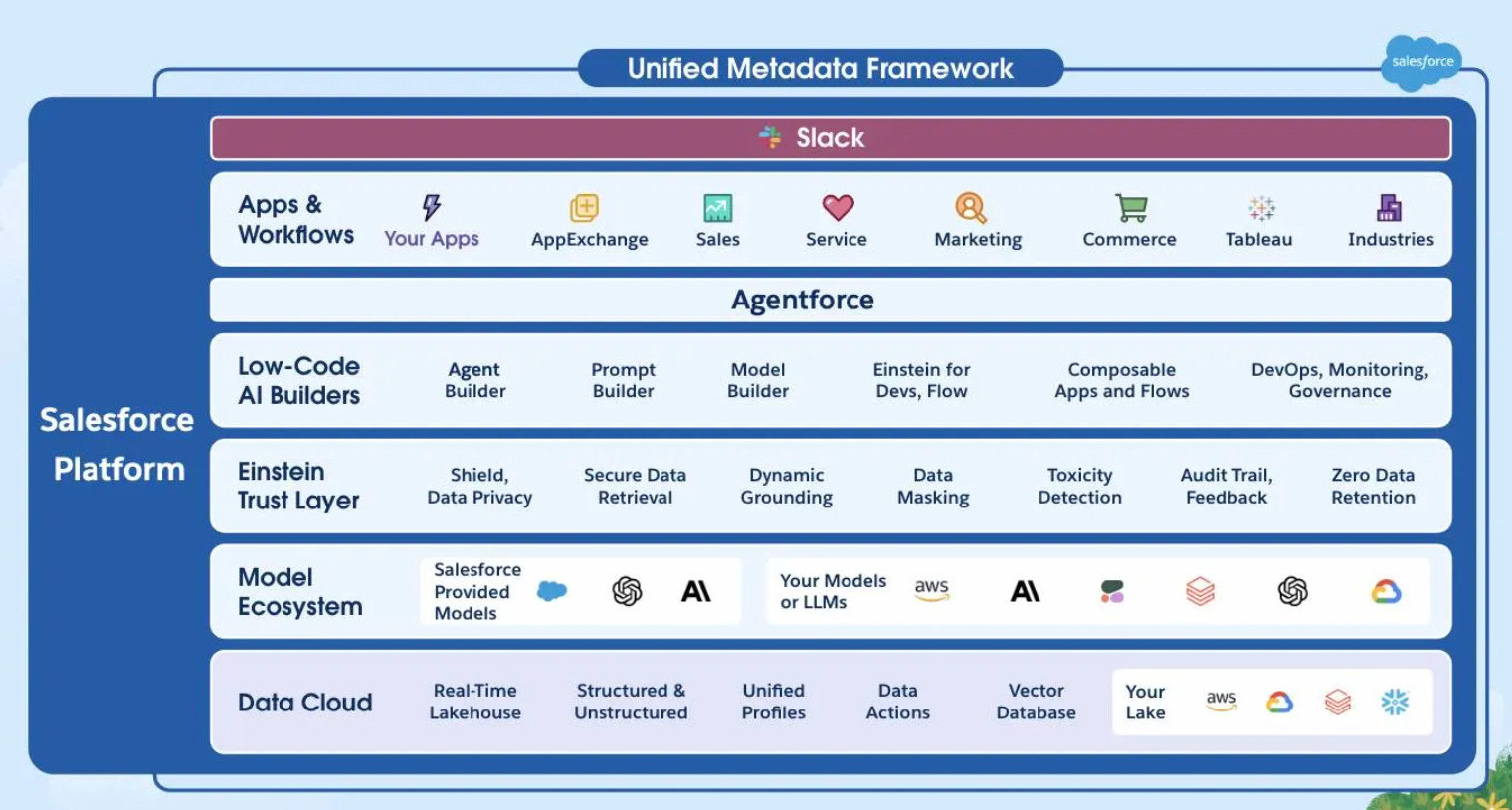

SaaS is not merely “software delivered via subscription.” It is an operating layer embedded into organizational workflows. Enterprise SaaS platforms such as Salesforce (CRM), Adobe (ADBE), ServiceNow (NOW), Workday (WDAY), and SAP (SAP) do not simply provide tools. They structure processes, enforce permissions, maintain audit trails, and encode business rules.

In other words, SaaS is not just functionality. It is institutional infrastructure.

Replacing SaaS would therefore require replacing:

Workflow orchestration

Data governance

Compliance structures

Role-based access control

Security and accountability layers

Integration across departments and systems

AI models, by themselves, do not inherently provide these capabilities. They generate probabilistic outputs. Enterprises require deterministic controls.

2. The Illusion of Replacement

The belief that AI replaces SaaS stems from a misunderstanding of how enterprises operate.

AI can:

Generate code

Summarize documents

Draft contracts

Produce images and marketing content

Answer questions over databases

However, most enterprise bottlenecks are not caused by a lack of content generation. They are caused by coordination costs, regulatory constraints, and cross-functional complexity.

An LLM can draft a sales email. It cannot replace a CRM system that:

Tracks multi-year customer relationships

Integrates billing and forecasting

Enforces compliance rules

Generates auditable records

AI improves tasks. SaaS structures processes.

This distinction matters.

3. AI as an Interface Layer

The more accurate framework is to view AI as an interface layer on top of SaaS, rather than a substitute for it.

Consider Salesforce. AI embedded within CRM does not eliminate the CRM. It reduces time spent on manual updates, surfaces risks in pipeline management, and summarizes account histories. The database, permissions architecture, and enterprise integrations remain indispensable.

Similarly, Adobe’s generative tools accelerate creative workflows, but they operate within a professional infrastructure that governs licensing, version control, brand compliance, and collaboration.

The economic value of AI inside SaaS is incremental but persistent:

Higher productivity per user

Increased feature depth

Higher switching costs

Expansion of average revenue per account

AI thickens the moat when embedded correctly.

4. Where AI Does Disrupt

This does not mean AI is neutral.

AI can and will disrupt:

Narrow, single-purpose SaaS tools

Feature-based point solutions

Products without proprietary data or workflow integration

Companies whose value proposition is primarily “automation of a simple task” are vulnerable. If a function can be commoditized by a general-purpose model with API access, pricing power compresses.

Examples of narrow SaaS vendors most exposed to AI substitution are typically companies built around a single functional layer rather than a system of record.

In marketing copy generation, platforms such as Jasper or Copy.ai originally differentiated themselves through templates and tone customization. However, once general-purpose LLMs became accessible through APIs and were embedded directly into platforms like Microsoft 365 (MSFT) or Google Workspace (GOOGL), much of that functional advantage narrowed. When text generation becomes a feature rather than a standalone product, pricing power compresses.

Similarly, résumé-building tools such as Rezi or lightweight AI meeting-summary tools like early versions of Otter.ai face pressure when summarization and drafting are natively integrated into Zoom, Google Meet, or Microsoft Teams ecosystems. The economic value shifts toward the platform that owns the workflow, not the feature that performs the task.

The winners are platforms that:

Control proprietary enterprise data

Own the workflow

Maintain distribution

Have compliance credibility

AI will pressure narrow, single-purpose SaaS tools whose value is essentially task automation. Standalone copywriting apps, basic chatbot providers, lightweight note summarizers, or simple workflow automators are structurally vulnerable. When a general-purpose model can perform most of the function through an API, differentiation erodes and pricing power compresses. Many feature-based tools in content marketing, entry-level analytics, or scheduling automation fall into this category.

By contrast, enterprise platforms such as Salesforce (CRM), Adobe (ADBE), ServiceNow (NOW), and SAP (SAP) are not defined by a single feature. They control proprietary enterprise data, own multi-layer workflows, and operate inside compliance-driven environments. AI may automate tasks within these systems, but it does not replace the system of record. In cybersecurity, for example, CrowdStrike (CRWD) benefits from AI-assisted analysis, yet the core value lies in telemetry, integration, and trust infrastructure.

AI compresses weak, feature-level vendors. It reinforces platforms that own data, workflow, and distribution.

5. Economic Structure: Cost Compression vs Revenue Expansion

AI affects SaaS economics through two channels.

Cost Compression

LLMs reduce:

Customer service costs

Onboarding friction

Documentation burden

Internal support workloads

This improves operating leverage.

Revenue Expansion

More interestingly, AI increases the depth of platform integration. When models are trained or fine-tuned using enterprise data, switching costs increase. The software becomes more embedded, not less.

This is why AI often strengthens incumbents rather than disrupts them. The firms that already control enterprise relationships and data flows are positioned to internalize AI gains.

6. The Commoditization Argument

Critics argue that if AI models become open and cheap, software layers collapse into thin wrappers.

This argument assumes that enterprise value lies in interface, not infrastructure.

But infrastructure is difficult to commoditize.

Compliance requirements, industry-specific workflows, regulatory constraints, and enterprise integrations cannot be replaced by a generic model. An AI may generate insight, but it cannot assume legal responsibility for execution.

Enterprises do not pay SaaS vendors for intelligence alone. They pay for reliability, accountability, uptime guarantees, and contractual obligations.

Ultimately, tools evolve, but agency remains human. The calculator replaced manual arithmetic, not mathematicians; Excel replaced paper ledgers, not accountants; the internet displaced print media, not the human need to create and interpret information. AI follows the same pattern. It augments productivity by providing better tools, but it does not eliminate the role of human judgment, coordination, and decision-making.

AI lacks liability. SaaS vendors assume it.

7. Capital Markets Perspective

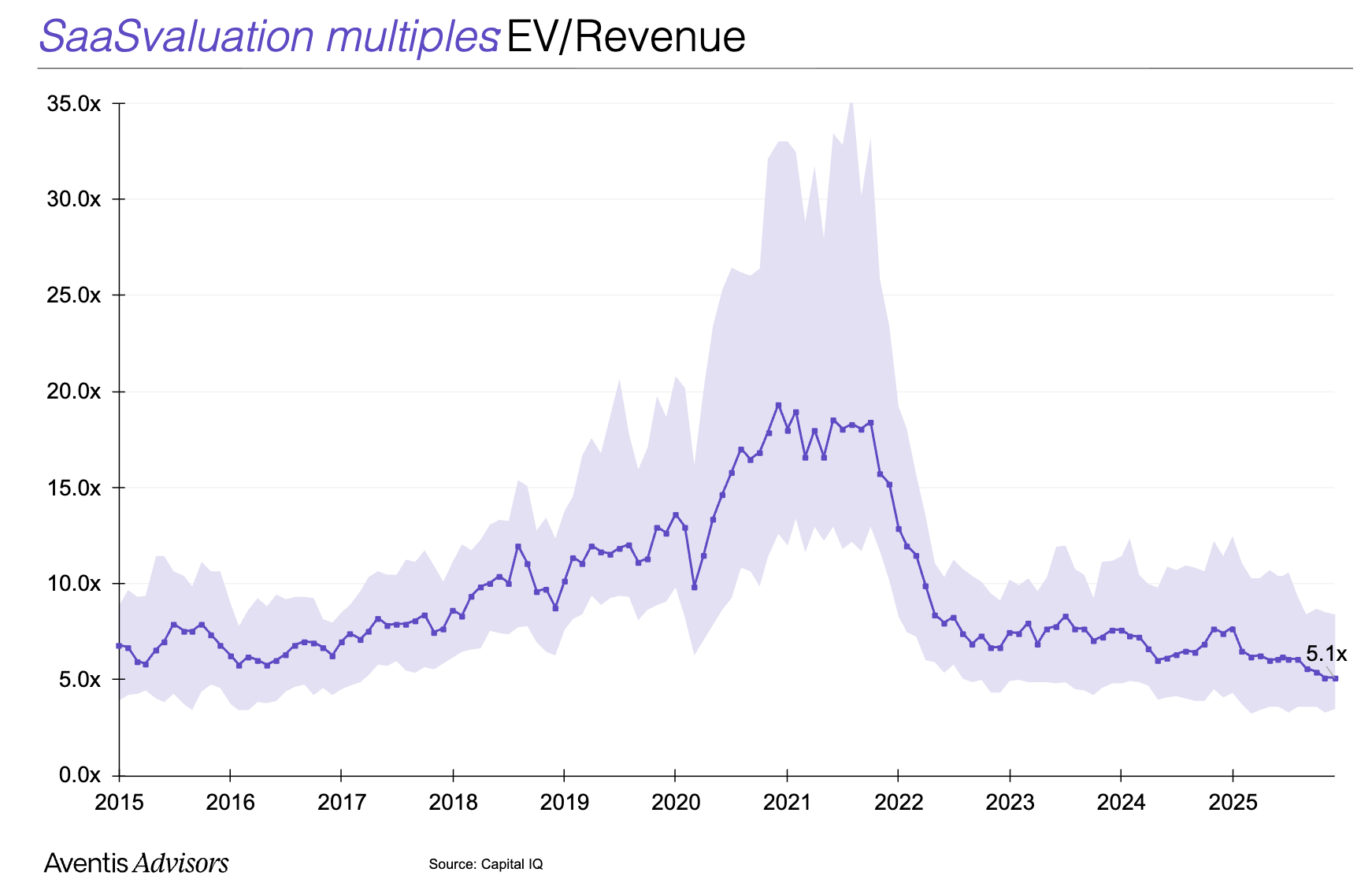

From a capital markets perspective, the “AI replaces SaaS” narrative has functioned less as a structural diagnosis and more as a catalyst for valuation compression. When a new general-purpose technology emerges, markets often assume incumbents face terminal risk before evidence of economic deterioration appears in financial statements. As a result, traditional enterprise software platforms are discounted on forward multiples long before recurring revenue streams show signs of instability.

However, earnings across many large SaaS platforms remain stable:

Recurring revenue models

High gross margins

Free cash flow generation

Embedded enterprise adoption

What typically adjusts first is growth expectation, not demand durability. Investors may lower terminal growth assumptions or compress multiples to reflect uncertainty around AI monetization. That repricing, however, should be distinguished from fundamental erosion of competitive position. AI-driven volatility reflects uncertainty about future industry structure. It does not automatically imply that current workflow ownership, switching costs, and contractual revenue are disappearing.

8. Boundaries of AI

Large language models are probabilistic systems. Enterprise environments are not.

AI produces outputs based on statistical likelihood. Corporations operate under legal accountability, regulatory oversight, contractual obligations, and financial reporting standards. A model may generate a plausible answer. An enterprise must generate a verifiable one.

This distinction is not philosophical. It is operational.

Models can hallucinate, misinterpret edge cases, or produce internally inconsistent outputs. In consumer contexts, this may be tolerable. In regulated industries such as finance, healthcare, insurance, or defense, it is not. Decisions must be traceable. Data lineage must be auditable. Access must be permissioned. Workflows must comply with jurisdictional rules.

Enterprise software exists precisely to impose structure on complexity. It defines data schemas, approval hierarchies, compliance checks, logging systems, and role-based access controls. These are not features that probabilistic models natively provide. They are governance layers built over time to reduce institutional risk.

AI becomes economically powerful when deployed inside these structured environments. Within defined guardrails, models can accelerate analysis, surface insights, and reduce cognitive friction. Outside those guardrails, they introduce uncertainty that enterprises cannot absorb.

SaaS platforms therefore function as boundary conditions. They constrain, validate, and document activity. AI augments the system, but the system provides the accountability.

The future of enterprise technology is unlikely to be model-only. It is far more likely to be model-within-structure.

9. A More Accurate Conclusion

AI does not replace SaaS. It reshapes SaaS.

The likely outcome is not elimination, but integration:

SaaS becomes AI-enhanced infrastructure

Weak vendors are absorbed or displaced

Strong platforms consolidate advantage

Pricing models evolve

Productivity increases

The enterprise stack becomes thinner at the surface and deeper at the core.

AI flattens certain tasks. It does not flatten institutional complexity.

10. Final Perspective

The more rigorous question is not whether AI replaces SaaS, but where economic value ultimately accumulates as AI becomes embedded across enterprises.

Technological history offers a consistent pattern. Foundational infrastructure tends to capture more durable economics than feature-level innovation. Early disruptors often generate excitement. Platform owners generate cash flow.

AI is undeniably transformative. It alters interfaces, compresses cognitive labor, and reduces certain coordination costs. Yet transformation does not automatically imply displacement. Most enterprise systems are not isolated tools; they are deeply integrated architectures that coordinate data, permissions, reporting, compliance, and institutional memory.

SaaS is not merely software functionality delivered over the cloud. It is the operating structure of modern organizations. It defines how data is stored, how workflows are executed, how accountability is enforced, and how decisions are recorded.

Architectures evolve incrementally. They absorb new layers. They integrate new interfaces. They rarely disappear overnight.

From an investment standpoint, the critical variable is durability of cash flow, not narrative intensity. AI will reshape enterprise software, but in many cases it will reinforce the position of platforms that already control workflow, data, and distribution.

So in short, AI might replace single function SaaS, but not the multi-layer SaaS with need of human involvement and human decision.

Disruption captures headlines. Durability compounds capital.

Disclaimer

This publication is provided for informational and educational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any securities. All opinions expressed are based on publicly available information believed to be reliable at the time of writing, but accuracy and completeness cannot be guaranteed. Past performance is not indicative of future results. Investing involves risk, including the potential loss of principal. Readers should conduct their own due diligence and consult a qualified financial advisor before making investment decisions.