The Risk Framework | Part One - Your Portfolio Architecture Is Your Risk Management

Most investors add risk controls after building their portfolio. The ones who compound consistently build risk management into the architecture from the beginning.

If you haven’t explored our previous research, you may revisit some of our earlier due diligence reports and thematic notes below. Each piece reflects the same thesis-driven framework we apply across every investment case.

For a closer look at how these principles translate into real positions, explore the 👉 Sample Portfolio — a demonstration of thesis-driven allocation and disciplined compounding.

What happens when you stop picking stocks and start building a system?

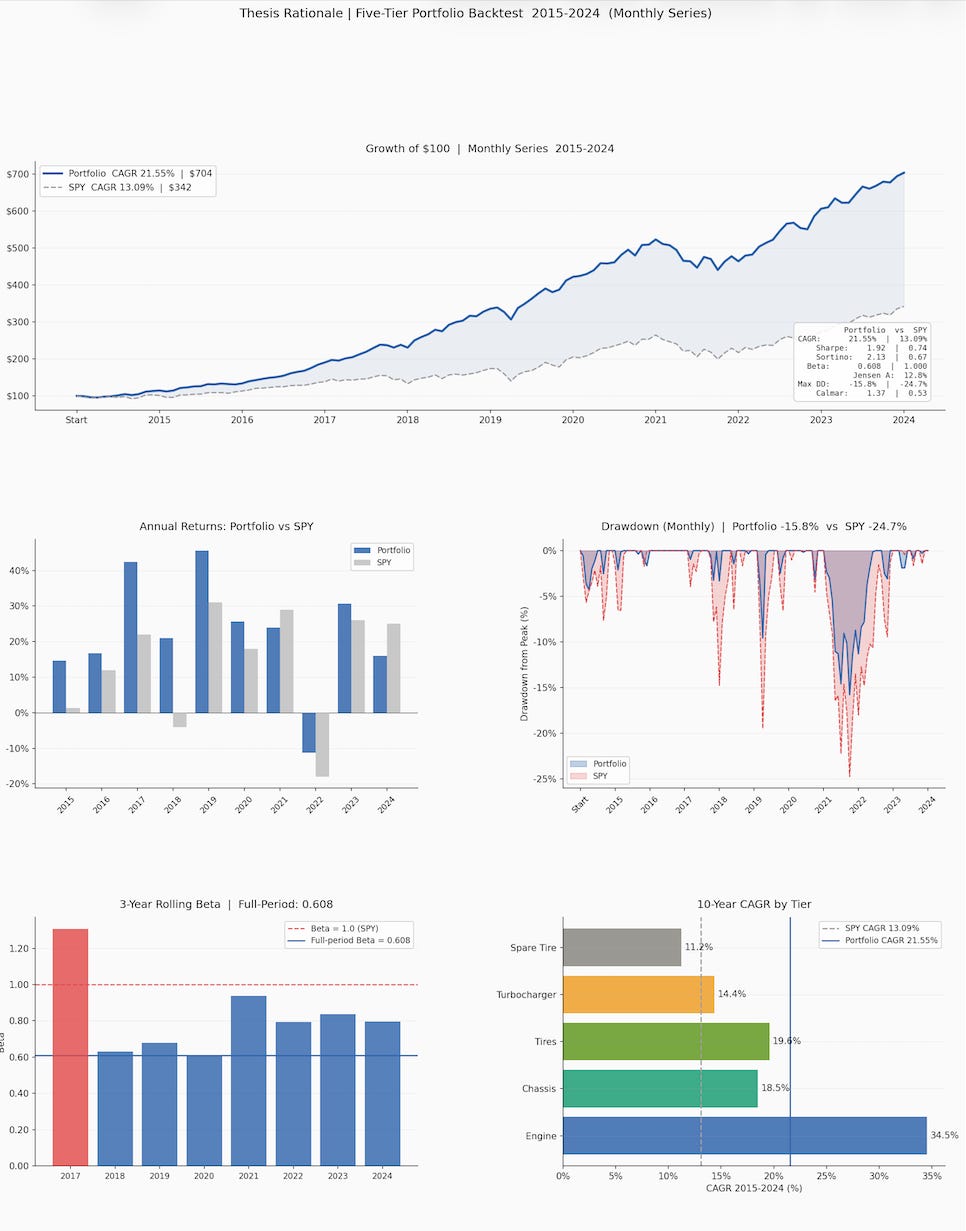

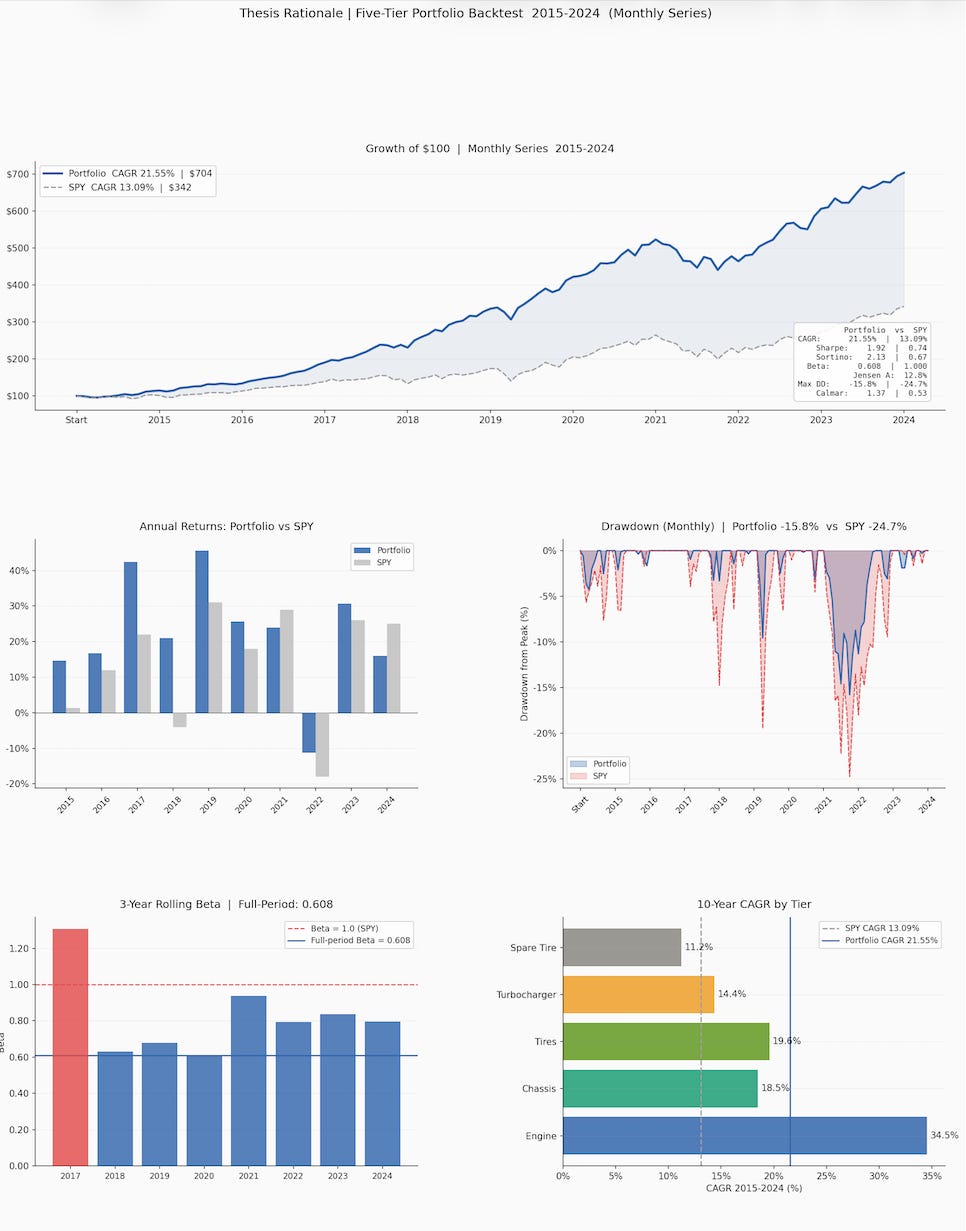

To stress-test this framework against a decade of real market conditions, we ran a quantitative backtest of the five-tier architecture from January 2015 through December 2024. The portfolio rebalances annually on January 1 of each year, with positions within each tier held at equal weight throughout the year. Monthly return series were derived from annual data using historically calibrated SPY monthly patterns and ticker-level correlations, allowing for a more realistic measurement of intra-year drawdowns and risk dynamics. The portfolio was constructed with the following testing allocation structure:

Tier 1 Engine (~30%)

Tier 2 Chassis (~20%)

Tier 3 Tires (~20%)

Tier 4 Turbocharger (~10%)

Tier 5 Spare Tire (~20%)

The results confirm the central thesis of this framework.

Return

Portfolio CAGR: 21.55% vs SPY 13.09%

$100 grew to $704 vs $342 for the index

Beat SPY in 8 out of 10 years

Risk-Adjusted Performance

Sharpe Ratio: 1.92 vs 0.74, nearly 2.6x the return per unit of volatility

Sortino Ratio: 2.13 vs 0.67, significantly stronger on a downside-adjusted basis

Jensen’s Alpha: 12.80% annualized after fully accounting for Beta exposure

Downside Control

Beta vs SPY: 0.608, the portfolio took on less than 61% of market systematic risk

Max Drawdown: -15.8% vs -24.7% for SPY, measured on a monthly basis

Worst single year: -11.3% in 2022, against SPY’s -18.0% in the same period

The architecture did not just generate higher returns. It generated higher returns while absorbing meaningfully less risk. That combination, lower Beta, lower drawdown, and higher risk-adjusted alpha, is precisely what the tiered structure was designed to produce. The five tiers that generated these numbers are not theoretical constructs. Each one has a specific job, and the data confirms that they did it.

Opening

There is a question that separates disciplined investors from reactive ones, and it is not about which stocks to buy. It is about what happens when everything goes wrong simultaneously.

In March 2020, the S&P 500 fell 34% in 33 days. In 2022, both equities and bonds declined together, eliminating the diversification benefit that most retail portfolios relied upon. In early 2025, a geopolitical shock sent energy prices surging while consumer confidence collapsed to a 70-year low. In each of these episodes, investors who had built reactive risk management systems, those who planned to hedge when conditions deteriorated, discovered that by the time they acted, the damage was already done. The VIX was already at 40. The puts were already expensive. The defensive rotation was already crowded.

The investors who navigated these periods without permanent capital impairment were not better forecasters. They were better architects. Their portfolios were designed, in advance, to absorb exactly the kind of stress those environments produced. Not because they predicted the specific events, but because they built systems that did not require prediction to function.

This is the first and most important principle of the Thesis Rationale Risk Framework: risk management is an architectural decision, not a monitoring function. It happens at the portfolio construction stage, not at the portfolio management stage. And the vehicle for that architecture is the tiered portfolio structure that organizes every position by the specific function it performs under stress.

Why Architecture Beats Hedging

Before examining how the tiered structure works, it is worth understanding why it is superior to the conventional approach of adding hedges reactively.

The conventional hedging approach has three structural problems that compound over time.

The first is timing. Protective instruments, whether put options, inverse ETFs, or volatility products, are most expensive precisely when they are most needed. When the VIX spikes from 15 to 40, the cost of buying protection has already tripled. The investor who waits for visible stress to hedge is systematically buying insurance at peak premium. Over a full market cycle, the cumulative cost of this timing mismatch is substantial.

The second is drag. An investor who maintains continuous protection against drawdowns pays a persistent cost in normal market conditions. A portfolio that spends 1% to 2% per year on protective instruments to avoid 15% to 20% drawdowns is making a mathematically poor trade in most environments, because the frequency of significant drawdowns does not justify the continuous cost of protection against them. The compounding drag of that insurance premium, applied year after year, destroys a meaningful fraction of the long-term return.

The third is behavioral. Reactive hedging creates a false sense of control that actually increases the likelihood of poor decisions. An investor who has purchased protection feels licensed to be more aggressive in their underlying positions, because they believe they are covered. When the protection expires or is removed, the underlying aggression remains. The hedge creates a moral hazard that makes the portfolio more dangerous, not less.

Architectural risk management avoids all three problems. Because the defensive properties are embedded in the businesses themselves rather than in derivative instruments layered on top of them, there is no timing problem, no drag, and no moral hazard. The defensive positions generate their own returns. They simply generate different returns under different conditions, which is precisely the diversification that a stress-resilient portfolio requires.

The Five-Tier Architecture and Its Risk Logic

The Thesis Rationale portfolio is organized into five functional tiers. Each tier performs a specific role in the overall risk architecture. Understanding what each tier is designed to do under stress is the foundation of understanding how the portfolio manages risk without requiring reactive decisions.

Tier One: The Engine

High-ROIC Compounders | Example Holdings: FICO, KNSL, CSU.TO, CPRT

The engine tier contains the businesses with the highest return on invested capital and the most durable compounding mechanisms. Its primary function in the risk architecture is not protection. It is the generation of excess returns over long periods that more than compensate for the volatility these businesses experience in the short term.

Understanding this distinction is critical. Engine businesses are not the most defensive positions in the portfolio. In a severe market correction, businesses like Copart or Constellation Software will experience meaningful price declines alongside the broader market. But their thesis does not break in a correction. Their competitive advantages do not erode because the VIX spiked or because the Federal Reserve delayed rate cuts. What happens in a correction is that they become available at better prices, which is why the engine tier is the primary destination for incremental capital during periods of market stress, not a source of defensive comfort.

The risk logic of the engine tier is long-duration. Its contribution to risk management is not in limiting short-term drawdowns but in ensuring that the portfolio’s compounding engine continues to run regardless of the macro environment. Kinsale Capital’s underwriting discipline does not change because energy prices are elevated. Constellation Software’s acquisition pipeline does not pause because consumer confidence has fallen. These businesses compound through cycles because their competitive advantages are structural, not cyclical.

The key risk monitoring variable for engine positions is thesis integrity, not price. The question to ask about every engine holding in every market environment is not “how much has it fallen?” but “has anything changed about the structural advantage that justified owning it?” If the answer is no, the appropriate response to a price decline is to hold, and potentially to add.

What breaks an engine position:

Sustained erosion of the competitive moat, such as a new entrant successfully replicating the business model at scale

A structural deterioration in the reinvestment opportunity, where ROIC falls persistently toward the cost of capital

A management decision that permanently impairs capital allocation quality, such as a large, overpriced acquisition that destroys the compounding mechanism

Price alone does not break an engine position. Fundamentals do.

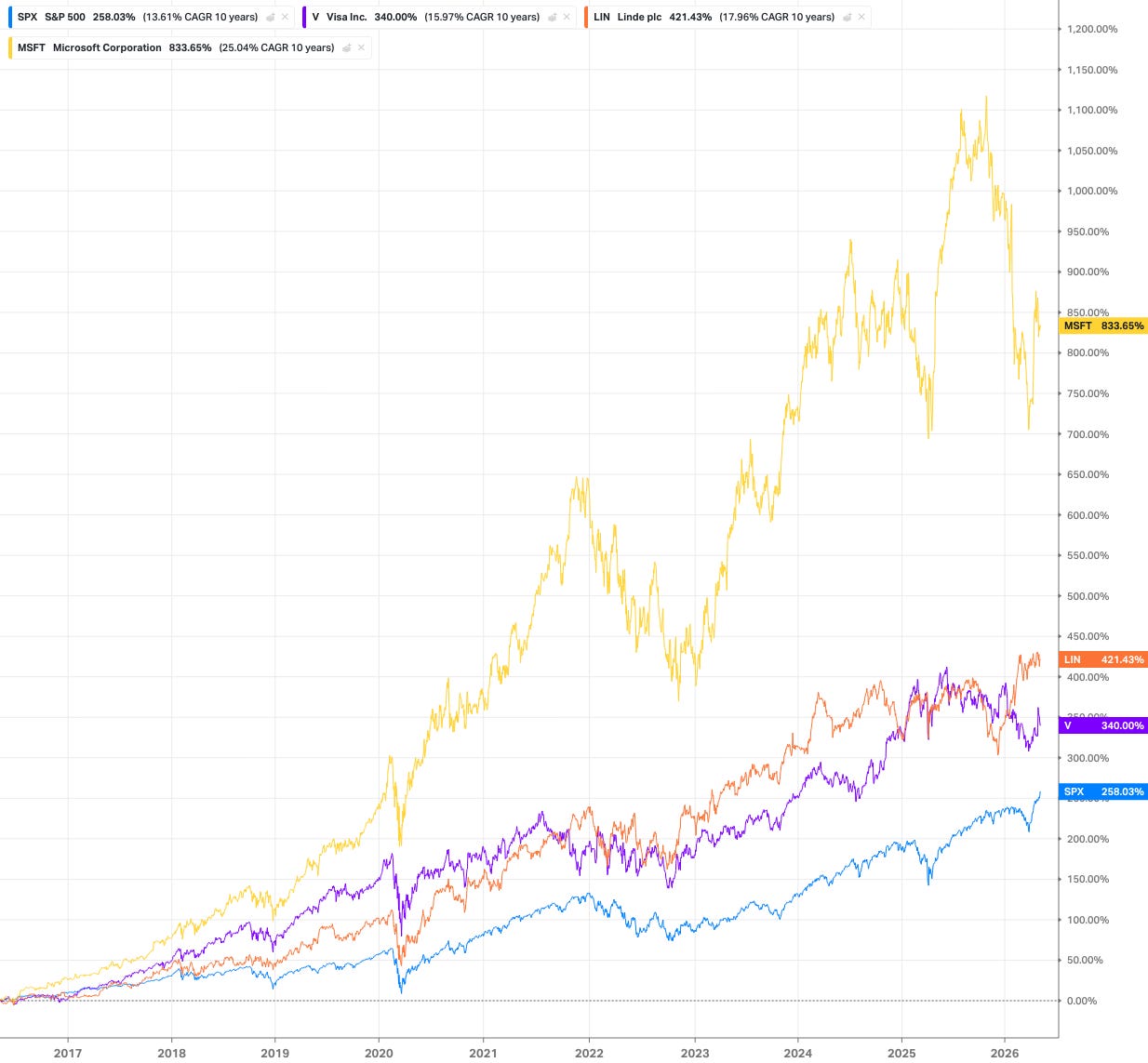

Tier Two: The Chassis

Structural Alpha | Example Holdings: V, MCO, LIN, MSFT

The chassis tier contains businesses so deeply embedded in the systems they serve that their revenue is structurally non-discretionary. These are not defensive businesses in the traditional sense of low volatility or low beta. They are businesses whose competitive position is protected by institutional embeddedness, regulatory recognition, or network effects so deep that the switching cost is not economic but operational.

Visa’s network processes transactions that must be processed. Moody’s ratings are required by investment mandates and regulatory frameworks. Linde’s industrial gases are mission-critical inputs under take-or-pay contracts. These are not preferences. They are requirements. And requirements do not pause because the macroeconomic environment is uncertain.

The chassis tier’s contribution to risk architecture is structural stability under prolonged stress. Where the engine tier generates long-term compounding, the chassis tier ensures the portfolio maintains its structural integrity during